St 105 Indiana PDF Form

St 105 Indiana PDF Form

Understanding the intricacies of tax exemption in the Hoosier State is crucial for registered retail merchants and businesses, both within and outside Indiana, aiming to conduct transactions free of sales tax. Recognized by the Indiana Department of Revenue, the Form ST-105, also known as the General Sales Tax Exemption Certificate, emerges as a vital document in this process. The form plays a pivotal role, demanding that users accurately declare their intention to purchase goods under a tax-exempt status—a privilege grounded in specific stipulations of the Indiana code. However, it’s important to note that this exemption strictly does not extend to utilities, vehicles, watercraft, or aircraft. The form stipulates that every section must be filled meticulously, as any omission could invalidate the exemption, forcing the purchaser to bear the sales tax, although a refund might be claimed later. Indiana’s rigorous in detailing that exemptions granted are in accord with their codes, explicitly disregarding the exemption statutes of other states for purchases from Indiana vendors. Hence, it’s essential for purchasers to provide either an Indiana Department of Revenue-issued Taxpayer Identification Number (TID) or, for those outside Indiana, a relevant state ID, among other specified identification alternatives. Moreover, the form doubles as a certification against misuse, simplifying tax-exempt purchases while sternly warning against fraudulent claims. In essence, Form ST-105 is a key to navigating Indiana’s sales tax exemptions, provided the document is filled out with utmost attention to detail, adhering strictly to the legislation in place.

Form |

Indiana Department of Revenue |

(R5 / |

General Sales Tax Exemption Certificate |

State Form 49065 |

|

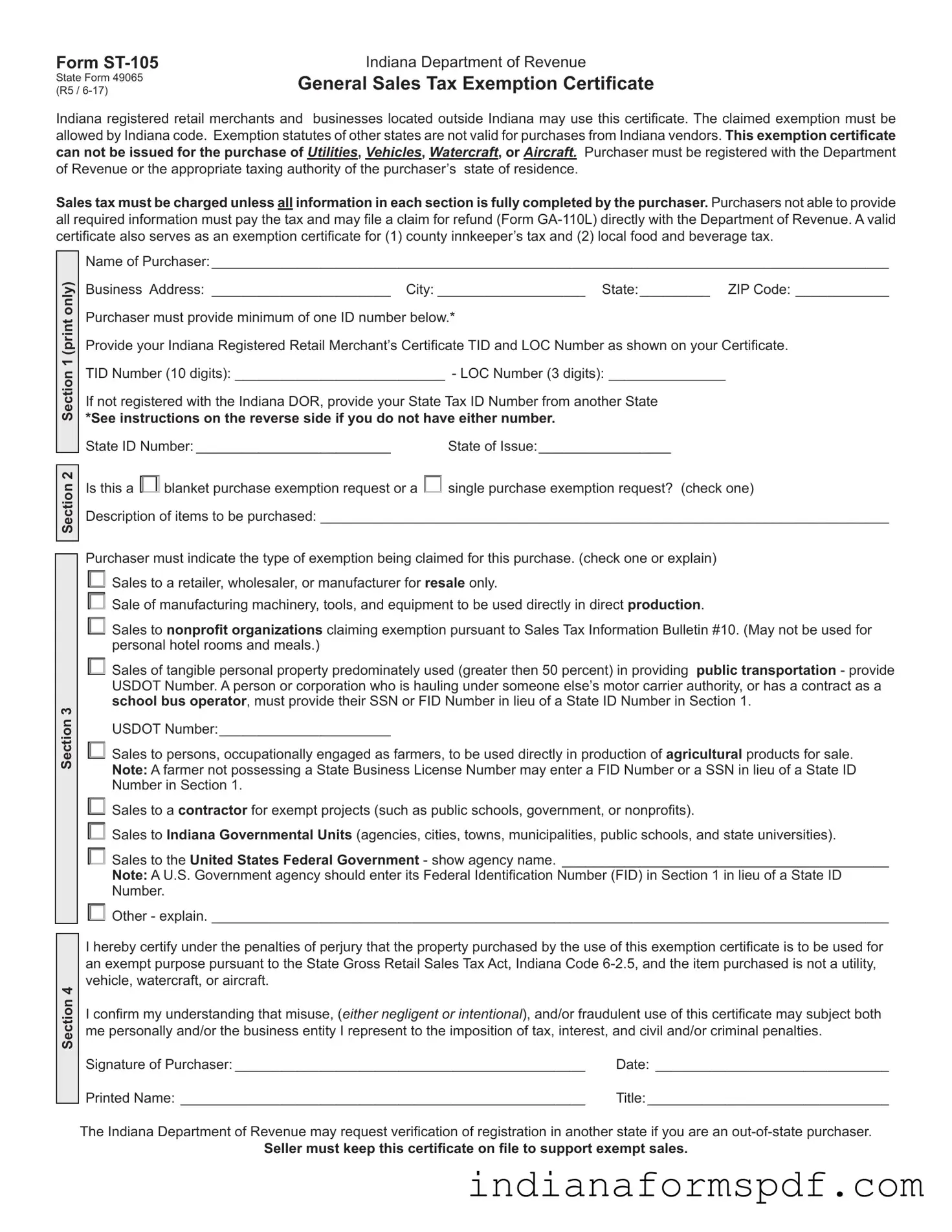

Indiana registered retail merchants and businesses located outside Indiana may use this certificate. The claimed exemption must be allowed by Indiana code. Exemption statutes of other states are not valid for purchases from Indiana vendors. This exemption certificate can not be issued for the purchase of Utilities, Vehicles, Watercraft, or Aircraft. Purchaser must be registered with the Department of Revenue or the appropriate taxing authority of the purchaser’s state of residence.

Sales tax must be charged unless all information in each section is fully completed by the purchaser. Purchasers not able to provide all required information must pay the tax and may file a claim for refund (Form

Section 2 Section 1 (print only)

Section 2 Section 1 (print only)

Section 3

Section 4

Name of Purchaser:________________________________________________________________________________________

Business Address:_ _______________________ City:____________________ State:__________ ZIP Code:_____________

Purchaser must provide minimum of one ID number below.*

Provide your Indiana Registered Retail Merchant’s Certificate TID and LOC Number as shown on your Certificate.

TID Number (10 digits):____________________________ - LOC Number (3 digits):________________

If not registered with the Indiana DOR, provide your State Tax ID Number from another State

*See instructions on the reverse side if you do not have either number.

State ID Number:__________________________ |

State of Issue:_________________ |

Is this a □blanket purchase exemption request or a □single purchase exemption request? (check one)

Description of items to be purchased:__________________________________________________________________________

□must indicate the type of exemption being claimed for this purchase. (check one or explain)

□Sales to a retailer, wholesaler, or manufacturer for resale only.

□Sale of manufacturing machinery, tools, and equipment to be used directly in direct production.

Sales to nonprofit organizations claiming exemption pursuant to Sales Tax Information Bulletin #10. (May not be used for

□personal hotel rooms and meals.)

Sales of tangible personal property predominately used (greater then 50 percent) in providing public transportation - provide USDOT Number. A person or corporation who is hauling under someone else’s motor carrier authority, or has a contract as a school bus operator, must provide their SSN or FID Number in lieu of a State ID Number in Section 1.

□USDOT Number:______________________

Sales to persons, occupationally engaged as farmers, to be used directly in production of agricultural products for sale. Note: A farmer not possessing a State Business License Number may enter a FID Number or a SSN in lieu of a State ID

□Number in Section 1.

□Sales to a contractor for exempt projects (such as public schools, government, or nonprofits).

□Sales to Indiana Governmental Units (agencies, cities, towns, municipalities, public schools, and state universities).

Sales to the United States Federal Government - show agency name._ __________________________________________

Note: A U.S. Government agency should enter its Federal Identification Number (FID) in Section 1 in lieu of a State ID

□Number. Other - explain.________________________________________________________________________________________Purchaser

I hereby certify under the penalties of perjury that the property purchased by the use of this exemption certificate is to be used for an exempt purpose pursuant to the State Gross Retail Sales Tax Act, Indiana Code

I confirm my understanding that misuse, (either negligent or intentional), and/or fraudulent use of this certificate may subject both me personally and/or the business entity I represent to the imposition of tax, interest, and civil and/or criminal penalties.

Signature of Purchaser:______________________________________________ |

Date:_ ______________________________ |

Printed Name:_____________________________________________________ |

Title:________________________________ |

The Indiana Department of Revenue may request verification of registration in another state if you are an

Seller must keep this certificate on file to support exempt sales.

Instructions for Completing Form

All four sections of the

Section 1

A)This section requires an identification number. In most cases this number will be an Indiana Department of Revenue issued Taxpayer Identification Number (TID - see note below) used for Indiana sales and/or withholding tax reporting. If the purchaser is from another state and does not possess an Indiana TID Number, a resident state’s business license, or State issued ID Number must be provided.

B)Exceptions - For a purchaser not possessing either an Indiana TID Number or another State ID Number, the following may be used in lieu of this requirement.

Federal Government – place your FID Number in the State ID Number space. Farmer – place your SSN or FID Number in the State ID Number space.

Public transportation haulers operating under another motor carrier authority, or with a contract as a school bus operator, must indicate their SSN or FID Number in the State ID Number space.

Nonprofit Organization – must show its FID Number in the State ID Number space.

Section 2

A)Check a box to indicate if this is a single purchase or blanket exemption.

B)Describe product being purchased.

Section 3

A)Purchaser must check the reason for exemption.

B)Purchaser must be able to provide additional information if requested.

Section 4

A)Purchaser must sign and date the form.

B)Printed name and title of signer must be shown.

Note: The Indiana Taxpayer Identification Number (TID) is a ten digit number followed by a three digit LOC Number. The TID is also known as the following:

a)Registered Retail Merchant Certificate

b)Tax Exempt Identification Number

c)Sales Tax Identification Number

d)Withholding Tax Identification Number

The Registered Retail Merchant Certificate issued by the Indiana Department of Revenue shows the TID (10 digits) and the LOC (3 digits) at the top right of the certificate.

| Fact | Detail |

|---|---|

| Name of Form | ST-105 Indiana General Sales Tax Exemption Certificate |

| Form Number | 49065 |

| Revision Date | R5 / 6-17 |

| Issuing Authority | Indiana Department of Revenue |

| Applicability | Indiana registered retail merchants and businesses located outside Indiana |

| Required Information | Purchaser's information, business identification numbers, exemption reason, and signature |

| Unique Requirements | Cannot be used for purchase of Utilities, Vehicles, Watercraft, or Aircraft |

| Governing Law | Indiana Code 6-2.5, State Gross Retail Sales Tax Act |

| Additional Eligibility | Includes exemptions for county innkeeper’s tax and local food and beverage tax |

Filling out the ST-105 Indiana General Sales Tax Exemption Certificate requires attention to detail and an understanding of your eligibility for the tax exemptions it offers. The significance of this process cannot be understated, as it directly impacts the taxation of purchases. Each step must be completed thoroughly to ensure the exemption is valid, preventing unwarranted charges of sales tax. It's an essential document for Indiana registered retail merchants or businesses located outside Indiana that are making tax-exempt purchases from Indiana vendors. The instructions below aim to provide clarity and ease the completion process.

After submitting the ST-105 form, it's important for both the purchaser and the seller to keep a copy on file. The seller in particular must retain this certificate to justify any exempt sales made under its authority. Should there be a need to verify the exemption, the Indiana Department of Revenue may request additional documentation, particularly from out-of-state purchasers. Therefore, maintaining accurate and accessible records of transactions made using this exemption certificate is vital for both parties.

What is the Form ST-105?

Form ST-105 is a General Sales Tax Exemption Certificate used by the Indiana Department of Revenue. It is for Indiana registered retail merchants and businesses located outside Indiana to document tax-exempt purchases. The claimed exemption must comply with Indiana code, not the exemptions statutes of other states.

Who can use Form ST-105?

Registered retail merchants with the Indiana Department of Revenue and businesses located outside of Indiana that are registered with their own state's taxing authority are eligible to use Form ST-105. It's important that the purchaser provides all required information to qualify for the exemption.

What purchases cannot be exempted using Form ST-105?

Form ST-105 cannot be used to exempt purchases of utilities, vehicles, watercraft, or aircraft. These categories are explicitly excluded from the exemptions allowed by the form.

Do I need to be registered to use Form ST-105?

Yes, the purchaser must be registered with either the Indiana Department of Revenue or the appropriate taxing authority of the purchaser’s state of residence. Without this registration, the sales tax exemption cannot be claimed using Form ST-105.

What happens if I cannot provide all the required information on Form ST-105?

If a purchaser cannot provide all the required information on the form, sales tax must be paid at the time of purchase. However, purchasers can file a claim for a tax refund directly with the Department of Revenue using Form GA-110L if they were entitled to an exemption but unable to claim it at the time of purchase.

Is Form ST-105 valid for a single purchase only?

No, Form ST-105 can be used for either a single purchase exemption or a blanket exemption, based on the selection made by the purchaser on the form. This makes it flexible for different purchasing needs.

Can Form ST-105 be used for personal purchases?

No, Form ST-105 is intended for business-related purchases that qualify for tax exemption under Indiana law. It cannot be used for personal items, personal hotel rooms, and meals.

What identification number is required on Form ST-105?

You must provide your Indiana Registered Retail Merchant’s Certificate TID and LOC Number if registered with Indiana DOR. If not registered in Indiana, you should provide your State Tax ID Number from another state. Certain exceptions apply, such as for government agencies or nonprofits, which can use their Federal Identification Number (FID).

What are the penalties for misuse of Form ST-105?

Misuse, whether negligent or intentional, or fraudulent use of this exemption certificate may subject both the individual and the business entity to tax, interest, as well as civil and/or criminal penalties, under the penalties of perjury.

How long must the seller keep Form ST-105?

The seller is required to keep the completed exemption certificate on file to support exempt sales. This is important for audit purposes, ensuring that the sale was legitimately tax-exempt according to the information provided on Form ST-105.

When it comes to handling the ST-105 Indiana General Sales Tax Exemption Certificate, it’s important to navigate the requirements carefully to ensure compliance and avoid common pitfalls. People often make mistakes in the process of completing this form due to oversight or misunderstanding of the instructions. Here are several areas where errors frequently occur:

To ensure compliance and the successful application of exemptions, carefully reviewing and understanding the instructions for completing the ST-105 Indiana form is essential. Attention to detail and providing accurate, complete information in every section will help avoid these common mistakes.

Lastly, it's important for both purchasers and sellers to retain a copy of the fully completed exemption certificate. This document is necessary for supporting exempt sales and may be required for verification by the Indiana Department of Revenue, especially for out-of-state purchasers. Ensuring the form is filled out correctly and retained for records plays a crucial role in maintaining compliance with Indiana sales tax laws.

When dealing with Form ST-105, the Indiana Department of Revenue General Sales Tax Exemption Certificate, individuals and businesses may need to complement it with other forms and documents to ensure compliance and proper record-keeping for tax purposes. These documents often collaborate to provide a comprehensive framework for tax exemption claims and verification, addressing the multifaceted nature of tax laws and regulations.

The documentation listed above enables various entities to substantiate their claims for tax exemptions, ensuring that all prerequisites are thoroughly met. By understanding the role of each accompanying form or document, businesses and individuals can navigate the complexities of tax exemption processes more effectively. It's essential for all involved parties to maintain accurate and up-to-date records of these documents to support their tax-related activities.

The ST-105 Indiana form, known as the General Sales Tax Exemption Certificate, aligns closely with exemption certificates in other states like the Resale Certificate used in states such as California and New York. Both forms serve similar primary functions: they allow registered retail merchants to purchase goods without paying sales tax, provided those goods are intended for resale. The Indiana ST-105 form requires the purchaser to detail their business information, including an identification number – either a Taxpayer Identification Number (TID) for Indiana-based businesses or a state-issued ID number for those outside Indiana. Similarly, the Resale Certificate mandates the provision of business details and the inclusion of a resale permit number or equivalent identifier. Both documents necessitate a declaration that the purchased items are for resale and not for personal use, underscoring their purpose in facilitating tax-free transactions between merchants.

Another document resembling the ST-105 is the Uniform Sales & Use Tax Certificate - Multijurisdiction, created by the Streamlined Sales Tax Governing Board. This multi-state form is designed to simplify the exemption certificate management process for vendors and purchasers involved in sales across multiple states. Like the ST-105, the Uniform Sales & Use Tax Certificate asks for detailed purchaser information, including business name, address, and a state-specific registration number. Both forms include a certification by the purchaser that the items bought are intended for resale, exempt use, or as ingredients or components of a new product. The central distinction lies in the multi-state applicability of the Uniform Certificate, contrasting the ST-105's specific use within Indiana. Nevertheless, both documents play pivotal roles in regulating sales tax exemptions across the U.S., ensuring compliance with state tax laws while facilitating business operations.

When filling out the ST-105 Indiana General Sales Tax Exemption Certificate, it's essential to approach the task with attention to detail to ensure its validity. Here are some key do's and don'ts to guide you through the process:

Remember, properly completing the ST-105 form is crucial not only for compliance with Indiana regulations but also for avoiding unnecessary tax liabilities. Misuse or fraudulent use of this exemption certificate may subject individuals or businesses to tax, interest, and civil or criminal penalties.

When it comes to the ST-105 Indiana General Sales Tax Exemption Certificate, there are several misconceptions that can lead to confusion and improper use of the form. Understanding these misconceptions is key to correctly applying for tax exemptions and avoiding potential penalties.

This is a common misunderstanding. In reality, the ST-105 is specifically designed for Indiana registered retail merchants and businesses located outside Indiana that are eligible for sales tax exemptions. These exemptions must be in accordance with Indiana code, and not every purchase or purchaser qualifies. It’s important that businesses meet the eligibility criteria and provide the necessary identification numbers to use this exemption certificate.

Actually, there are specific limitations on what can be purchased tax-free with this form. Purchases of utilities, vehicles, watercraft, or aircraft are explicitly excluded from tax exemption using the ST-105 form. The form is predominantly used for items that are for resale or for use in manufacturing, agricultural production, or in providing exempt services like public transportation.

This is not entirely true. While having an Indiana Department of Revenue issued Taxpayer Identification Number (TID) is the standard requirement, there are exceptions. For example, if a purchaser is based out of state and doesn’t possess an Indiana TID, they can provide their State issued ID Number from their state of residence. Other exceptions include federal government purchasers using a Federal Identification Number (FID) or farmers using their SSN or FID in lieu of a state business license number.

Some might think that if they are eligible for an exemption, simply not charging the tax is sufficient. However, to properly execute a tax-exempt transaction, it's mandatory to complete all four sections of the ST-105 form accurately. Failure to do so can result in the seller being held responsible for the uncollected tax. A fully completed form serves as documentation that supports the tax-exempt sale and protects both the seller and the purchaser from potential tax liability issues.

Understanding these misconceptions and the accurate requirements of the ST-105 Indiana General Sales Tax Exemption Certificate is essential for businesses seeking tax exemptions on eligible purchases. When in doubt, referencing the detailed instructions provided with the form or consulting with the Indiana Department of Revenue can help ensure compliance and correct application of tax exemptions.

Filling out the ST-105 Indiana General Sales Tax Exemption Certificate requires attention to detail and an understanding of the exemptions provided by Indiana code. Here are ten key takeaways for effectively completing and using this form:

Understanding these key points ensures that businesses can navigate the complexities of sales tax exemptions in Indiana, fostering compliance and operational efficiency.

Indiana Legal Forms Free - Acts as a linchpin for initiating legal actions in civil court, representing the first formal step in the litigation process.

Indiana Deer Hunting Hours - A necessary step for any hunter wishing to use private land, providing clarity and legal protection, and ensuring that hunting activities are respectful of property boundaries.