Indiana State 104 PDF Form

Indiana State 104 PDF Form

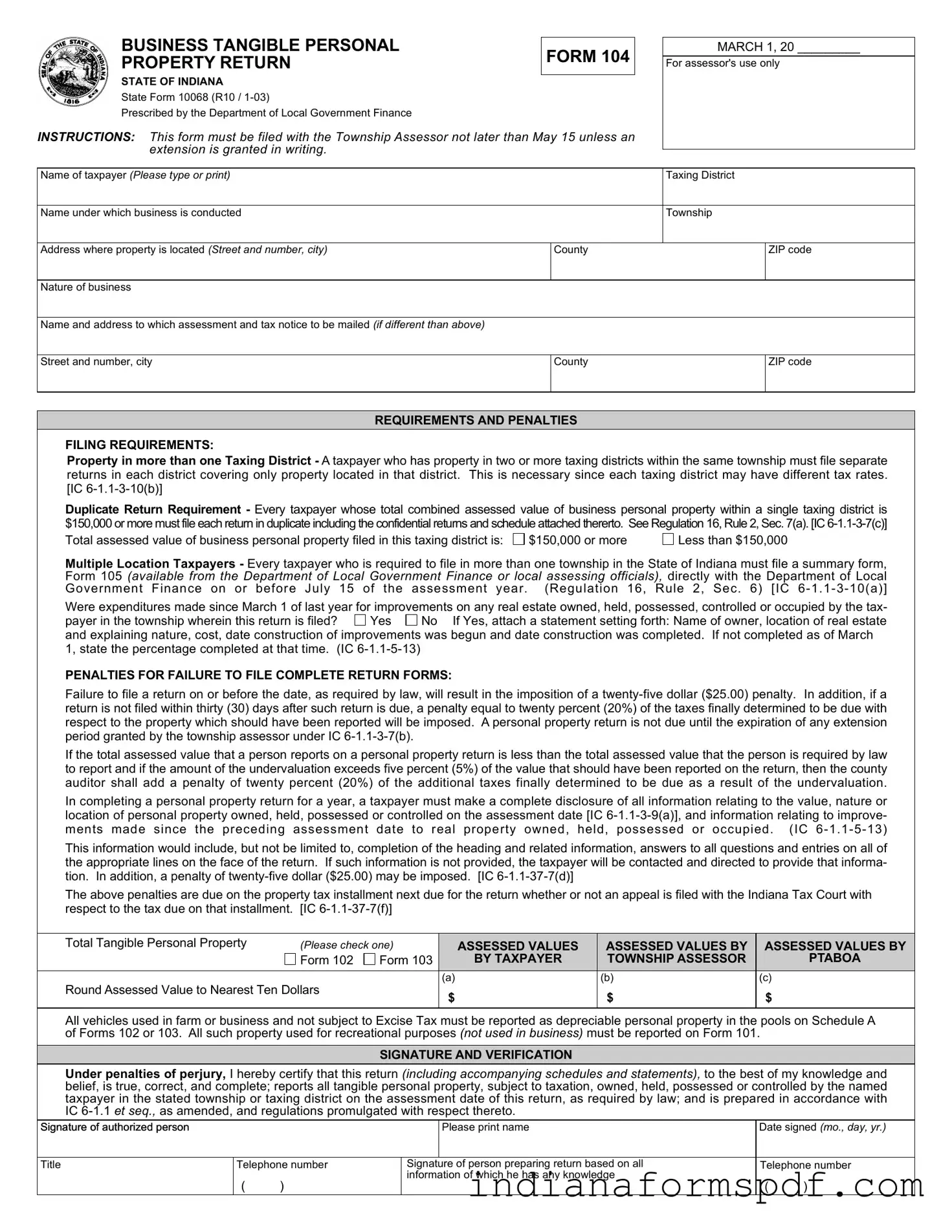

In the heartland of America, the State of Indiana requires businesses to navigate the complexities of tax compliance with the Indiana State 104 form, a critical component in maintaining transparency and accountability in business tangible personal property taxation. Characterized by a comprehensive structure, this form serves as a declaration of business personal property held within the state, ensuring that businesses contribute fairly to local economies through property tax. Mandatory to be filed with the Township Assessor by May 15, unless an extension is graciously granted, the form seeks to collate detailed information regarding the taxpayer's assets, including but not limited to the nature of the business, location, and the assessed value of tangible personal property. This instrument of financial governance not only delineates the specifics of filing requirements, catering to businesses with assets in multiple taxing districts or possessing property valued over $150,000, but also lays out the consequences for non-compliance, including significant penalties. Such penalties are meticulously outlined to ensure adherence to regulations, with the possibility of fines for incomplete returns or underreporting of property values, emphasizing the importance of accuracy and completeness. The form, prescribed by the Department of Local Government Finance, embodies a critical exercise in fiscal responsibility, guiding businesses through the nuances of property tax obligations while fostering an environment of fairness and equity in tax administration.

BUSINESS TANGIBLE PERSONAL |

FORM 104 |

|

PROPERTY RETURN |

||

|

||

|

|

STATE OF INDIANA

State Form 10068 (R10 /

Prescribed by the Department of Local Government Finance

INSTRUCTIONS: This form must be filed with the Township Assessor not later than May 15 unless an extension is granted in writing.

MARCH 1, 20 _________

For assessor's use only

Name of taxpayer (Please type or print) |

|

Taxing District |

|

|

|

|

|

Name under which business is conducted |

|

Township |

|

|

|

|

|

Address where property is located (Street and number, city) |

County |

|

ZIP code |

|

|

|

|

Nature of business |

|

|

|

|

|

|

|

Name and address to which assessment and tax notice to be mailed (if different than above) |

|

|

|

|

|

|

|

Street and number, city |

County |

|

ZIP code |

|

|

|

|

REQUIREMENTS AND PENALTIES

FILING REQUIREMENTS:

Property in more than one Taxing District - A taxpayer who has property in two or more taxing districts within the same township must file separate returns in each district covering only property located in that district. This is necessary since each taxing district may have different tax rates. [IC

Duplicate Return Requirement - Every taxpayer whose total combined assessed value of business personal property within a single taxing district is $150,000 or more must file each return in duplicate including the confidential returns and schedule attached thererto. See Regulation 16, Rule 2, Sec. 7(a). [IC

Total assessed value of business personal property filed in this taxing district is:

$150,000 or more

Less than $150,000

Multiple Location Taxpayers - Every taxpayer who is required to file in more than one township in the State of Indiana must file a summary form, Form 105 (available from the Department of Local Government Finance or local assessing officials), directly with the Department of Local Government Finance on or before July 15 of the assessment year. (Regulation 16, Rule 2, Sec. 6) [IC

Were expenditures made since March 1 of last year for improvements on any real estate owned, held, possessed, controlled or occupied by the tax- payer in the township wherein this return is filed?  Yes

Yes  No If Yes, attach a statement setting forth: Name of owner, location of real estate and explaining nature, cost, date construction of improvements was begun and date construction was completed. If not completed as of March 1, state the percentage completed at that time. (IC

No If Yes, attach a statement setting forth: Name of owner, location of real estate and explaining nature, cost, date construction of improvements was begun and date construction was completed. If not completed as of March 1, state the percentage completed at that time. (IC

PENALTIES FOR FAILURE TO FILE COMPLETE RETURN FORMS:

Failure to file a return on or before the date, as required by law, will result in the imposition of a

If the total assessed value that a person reports on a personal property return is less than the total assessed value that the person is required by law to report and if the amount of the undervaluation exceeds five percent (5%) of the value that should have been reported on the return, then the county auditor shall add a penalty of twenty percent (20%) of the additional taxes finally determined to be due as a result of the undervaluation.

In completing a personal property return for a year, a taxpayer must make a complete disclosure of all information relating to the value, nature or location of personal property owned, held, possessed or controlled on the assessment date [IC

This information would include, but not be limited to, completion of the heading and related information, answers to all questions and entries on all of the appropriate lines on the face of the return. If such information is not provided, the taxpayer will be contacted and directed to provide that informa- tion. In addition, a penalty of

The above penalties are due on the property tax installment next due for the return whether or not an appeal is filed with the Indiana Tax Court with respect to the tax due on that installment. [IC

Total Tangible Personal Property |

(Please check one) |

|

ASSESSED VALUES |

ASSESSED VALUES BY |

ASSESSED VALUES BY |

|

|

Form 102 |

Form 103 |

|

BY TAXPAYER |

TOWNSHIP ASSESSOR |

PTABOA |

|

|

|

(a) |

|

(b) |

(c) |

Round Assessed Value to Nearest Ten Dollars |

|

$ |

|

$ |

$ |

|

|

|

|

|

|||

|

|

|

|

|

|

|

All vehicles used in farm or business and not subject to Excise Tax must be reported as depreciable personal property in the pools on Schedule A of Forms 102 or 103. All such property used for recreational purposes (not used in business) must be reported on Form 101.

SIGNATURE AND VERIFICATION

Under penalties of perjury, I hereby certify that this return (including accompanying schedules and statements), to the best of my knowledge and belief, is true, correct, and complete; reports all tangible personal property, subject to taxation, owned, held, possessed or controlled by the named taxpayer in the stated township or taxing district on the assessment date of this return, as required by law; and is prepared in accordance with IC

Signature of authorized person |

|

|

|

Please print name |

Date signed (mo., day, yr.) |

|

|

|

|

|

|

||

Title |

Telephone number |

Signature of person preparing return based on all |

Telephone number |

|||

|

( |

) |

information of which he has any knowledge |

|

|

|

|

|

|

( |

) |

||

| Fact Name | Detail |

|---|---|

| Form Type | Indiana State Form 104 - Business Tangible Personal Property Return |

| Prescribing Authority | Department of Local Government Finance |

| Form Number | State Form 10068 (R10 / 1-03) |

| Filing Deadline | Must be filed with the Township Assessor on or before May 15 unless an extension is granted in writing. |

| Governing Laws for Filing Requirements | IC 6-1.1-3-10(b), IC 6-1.1-3-7(c), and IC 6-1.1-3-10(a) |

| Penalty for Late Filing | A penalty of $25.00 is imposed for failing to file a return on time, with further penalties up to 20% of the taxes due for filings more than 30 days late or for undervalued reporting. |

| Undervaluation Penalty | If the reported total assessed value is less than it should be by more than 5%, a penalty of 20% of the additional taxes determined to be due is added. |

| Signature Requirement | The return requires the signature of an authorized person certifying under penalties of perjury that the return is complete and accurate. |

Filling out the Indiana State 104 Form is a crucial step for taxpayers in Indiana to accurately report their business tangible personal property. Ensuring that this form is completed accurately and submitted by the May 15 deadline is vital to comply with state requirements and avoid potential penalties. The instructions here aim to simplify the process, breaking down the form into manageable steps to ensure clarity and compliance.

Once the form is correctly filled out, it should be submitted to the Township Assessor on or before the May 15 deadline. Filing this form on time helps ensure that your business complies with Indiana's regulations regarding business tangible personal property. Careful and accurate completion of the form is necessary to avoid penalties for late filing or inaccurate reporting. Should the need arise for an extension, it must be requested in writing from the Township Assessor before the deadline. Compliance with these procedures ensures that the assessment process moves forward smoothly.

What is the Indiana State 104 form?

The Indiana State 104 form is the Business Tangible Personal Property Return for the state of Indiana. It's a document used by businesses to report personal property used in the business for taxation purposes. This includes information about the nature and value of the property they own, hold, possess, or control within a specific township or taxing district in Indiana.

When is the deadline to file the Indiana State 104 form?

This form must be filed with the Township Assessor no later than May 15, unless a written extension has been granted. It's important for businesses to meet this deadline to avoid penalties.

Who needs to file this form?

Any business that owns, holds, possesses, or controls tangible personal property within a township or taxing district in the State of Indiana must file this form. This includes businesses with property in multiple taxing districts within the same township, which must file separate returns for each district.

Are there any requirements for businesses with property in multiple locations?

Yes, businesses required to file in more than one township in the state must also submit a summary form, Form 105, to the Department of Local Government Finance by July 15 of the assessment year. This is in addition to the individual returns for each district where the property is located.

What if my business has made improvements to real estate?

If your business has made expenditures for improvements on real estate since March 1 of the previous year, you must attach a statement to your return. This statement should include the owner's name, location of the real estate, and details about the nature, cost, and dates of the construction of improvements.

What are the penalties for failure to file or incomplete filings?

Failure to file this form by the due date will result in a $25.00 penalty. Additionally, if a return is not filed within 30 days after it is due, a penalty of 20% of the taxes determined to be due on the property that should have been reported will be imposed. An undervaluation penalty of 20% of the additional taxes may also be applied if the reported value is significantly less than the required amount.

How is the assessed value calculated and reported?

On the form, taxpayers must declare the assessed value of their business personal property, rounding the value to the nearest ten dollars. They will indicate whether this value has been assessed by the taxpayer, township assessor, or PTABOA. All business and farm vehicles not subject to Excise Tax must also be reported as depreciable personal property.

What is the verification process for the form?

The form requires a signature under penalties of perjury, certifying that the return is true, correct, and complete to the best of the filer's knowledge. It verifies that all tangible personal property subject to taxation and controlled or possessed by the taxpayer in the stated township or taxing district as of the assessment date is reported as required by law.

Filling out the Indiana State 104 form, known as the Business Tangible Personal Property Return, is a routine yet crucial task for business owners in Indiana. It requires careful attention to detail, as mistakes can lead to penalties, increased tax liabilities, or other legal complications. Here are nine common errors people make when completing this form:

Avoiding these mistakes requires a detailed review process and an understanding of the form's requirements. Business owners should consider consulting with a tax professional to ensure compliance and to navigate the complexities of property tax filing. Remember, the goal is to accurately report business personal property to avoid penalties and ensure the correct tax assessment, supporting a fair and equitable tax system in Indiana.

In conclusion, while the process of filling out the Indiana State 104 form might seem straightforward, the potential for errors is significant. The repercussions of these mistakes can be more than just financial; they can also take up valuable time and resources to correct. Taking the time to double-check your return, understanding the specifics of the filing requirements, and staying on top of deadlines helps ensure smooth sailing in the realm of business personal property taxation in Indiana.

Filing the Indiana State Form 104, also known as the Business Tangible Personal Property Return, is a critical step for businesses to appropriately declare their taxable property within the state. This form requires accurate and comprehensive disclosure of tangible personal property for tax purposes. To ensure compliance and accuracy, other documents and forms are often used in conjunction with Form 104. These documents support the detailed reporting and verification processes required by the Indiana Department of Local Government Finance and aid in the accurate assessment of a business's taxable property.

Together, these documents ensure that businesses provide a comprehensive and accurate depiction of their taxable personal property. Each form and report plays a distinct role in helping businesses navigate the complexities of property tax reporting and compliance, ultimately ensuring that taxpayers meet their obligations under Indiana law. By fully understanding and utilizing these forms, businesses can achieve compliance, minimize errors, and accurately report their tangible personal property for taxation purposes.

The Indiana State 104 form, known as the Business Tangible Personal Property Return, shares similarities with a variety of other legal documents, specifically in its function of assessing and reporting property for tax purposes. Here are a few such documents and how they compare:

Form 102 - Personal Property Return: Both the Indiana State 104 and Form 102 serve to report business personal property, albeit with slight differences in their scopes. Form 102 is generally aimed at reporting personal property for businesses, such as equipment and machinery, to assess their taxable value. The key similarity lies in their purpose: to calculate tax based on the value of business-owned personal property. However, Form 102 is broader in scope, covering a wider range of personal property items.

Form 103 - Short Form - Personal Property Return: The Form 103, or the Short Form, is a streamlined version of personal property reporting forms, designed for smaller businesses or those with simpler asset portfolios. Like the Indiana State 104, it is used to report and assess the value of personal property for taxation purposes. The main similarity is their intent to ensure businesses pay their fair share of taxes based on the value of their tangible assets. The difference lies in the form's complexity and the detail required, with the 103 Form being less comprehensive.

Form 105 - Multiple Location Return: This document is specifically for taxpayers who need to report personal property across multiple locations within Indiana. Similar to the Indiana State 104, Form 105 deals with the complexities of assessing property value for tax purposes but focuses on the logistics of owning property in more than one taxing district. Both forms are integral to the accurate reporting and taxation process for business assets, ensuring that each location is accounted for in the taxpayer’s annual obligations.

When dealing with the Indiana State Form 104 for Business Tangible Personal Property Return, attention to detail is crucial to ensure accuracy and compliance with state regulations. Here's a guide to help you navigate this process effectively:

What You Should Do:

What You Shouldn't Do:

When discussing the Indiana State 104 form, also known as the Business Tangible Personal Property Return, several misconceptions can lead to confusion and potential errors for taxpayers. Here's a list of common misunderstandings and the clarifications to help ensure accurate and compliant submissions.

Every business needs to file a Form 104 annually. This isn't always the case. Only businesses with tangible personal property used in their operations in Indiana are required to file.

The filing deadline is always May 15. In fact, the deadline may be extended by the Township Assessor, and businesses should verify the current year's deadline.

Form 104 is the only form needed for business personal property taxation. Not quite. Depending on the situation, additional forms like Form 105 for multi-location taxpayers or confidential schedules may be required.

If you haven’t made any new purchases, you don’t need to file. Incorrect. The form must be filed every year, regardless of whether new tangible personal property has been acquired.

The form is complicated and requires professional assistance to complete. While it's comprehensive, many businesses fill out the form without external help. The key is to thoroughly read instructions and understand your business's assets.

Only physical goods count as tangible personal property. Actually, it also includes other items like machinery, equipment, and any property that is not real estate but is used in your business.

Filing the form late doesn’t carry any penalties. This is not true. Late filings can result in monetary penalties, and failing to disclose all relevant property may lead to additional taxes and fines.

The form must be filed only at the state level. Incorrect. It must be filed with the local Township Assessor, and requirements can vary by locality within Indiana.

All businesses file the same version of the form. Not necessarily. The total combined assessed value of business personal property dictates whether a business files the return in duplicate or needs additional schedules attached.

You can't request an extension for filing the form. In reality, extensions can be granted, but they must be requested in writing from the Township Assessor.

Understanding these points can help businesses in Indiana approach the Form 104 filing process more confidently and compliantly. It's essential to recognize the significance of accurately reporting business personal property to avoid unnecessary complications with local taxing authorities.

Filing the Indiana State 104 form is a key responsibility for business owners with tangible personal property in Indiana. Understanding the essential takeaways can streamline the process and help avoid common pitfalls. Here are seven key aspects to remember:

Thoroughly understanding these points ensures compliance and helps prevent unnecessary penalties or complications with your business's tangible personal property assessment in Indiana.

Indiana Department of Unemployment - Employers unable to register online must attach this form to their first quarterly contribution report.

Indiana St 103 - Provides a structured method for Indiana businesses to track sales, exemptions, and calculate net taxable sales monthly.

What Is a Financial Declaration - Plays a critical role in determining equitable spousal maintenance arrangements.