Indiana St 105 PDF Form

Indiana St 105 PDF Form

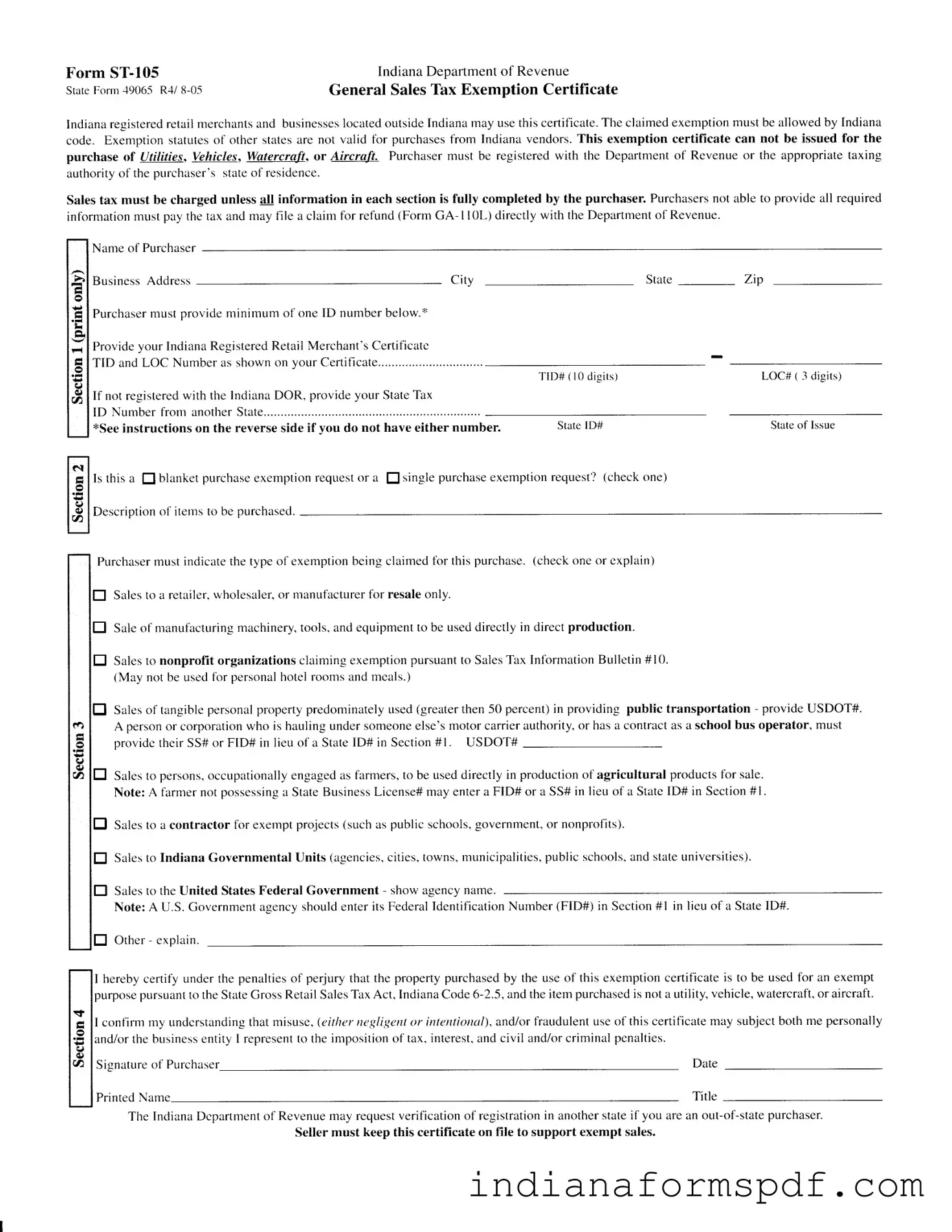

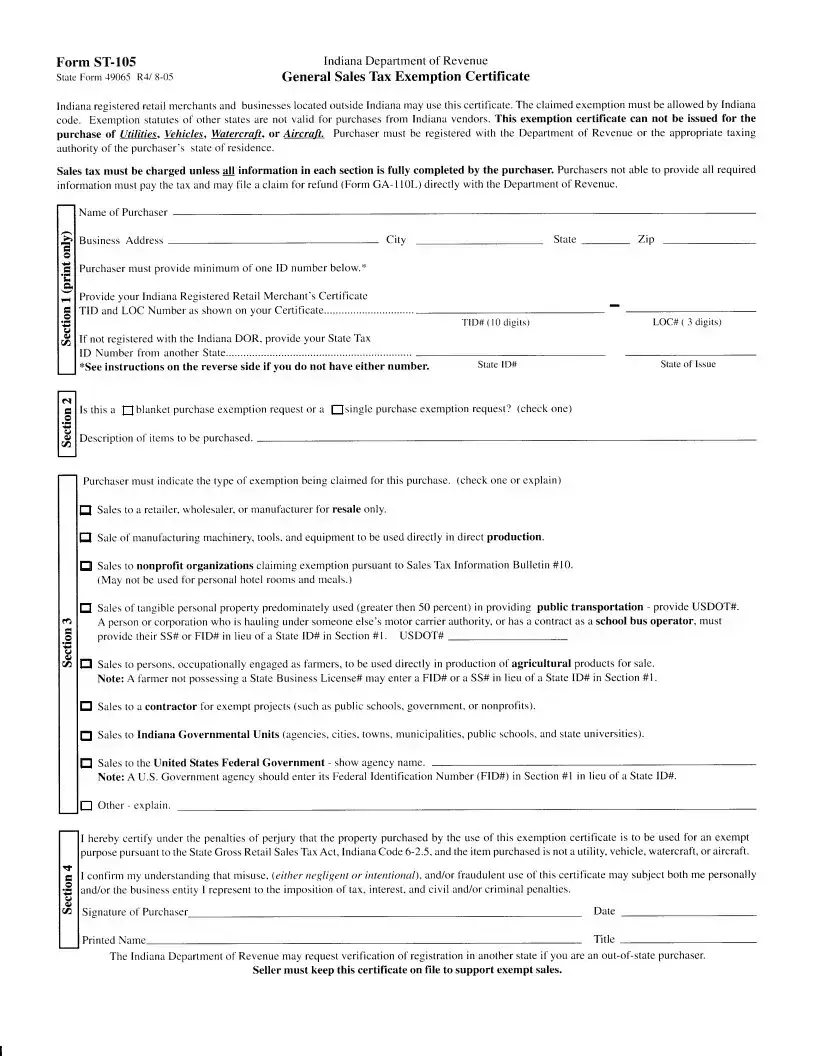

The Indiana ST-105 form, also known as the General Sales Tax Exemption Certificate, serves a crucial role for Indiana-registered retail merchants and businesses located outside Indiana, who seek to buy products tax-exempt for specific purposes. These businesses must ensure that their purchases align with Indiana Code allowances for tax exemption, emphasizing that exemptions applicable in other states do not hold validity for Indiana-based transactions. Notably, the form specifies that exemptions cannot be applied to utilities, vehicles, watercraft, or aircraft purchases. For a transaction to be considered tax-exempt, every section of the form requires complete and accurate information from the purchaser, including identification numbers that can either be an Indiana Department of Revenue issued Taxpayer Identification Number (TID#) or a state-issued ID number from another state if the purchaser is not registered with the Indiana DOR. Additionally, in certain circumstances, other numbers like a Federal Identification Number (FID#) or Social Security Number (SS#) can be substituted, catering to specific entities like farmers, public transportation haulers, or non-profit organizations. The form also mandates the purchaser to specify the type of exemption being claimed through a selection of predefined criteria or an explanation if the exemption falls under an 'Other' category. Misuse or fraudulent use of this certificate may subject the users to tax liabilities, including interest and possible civil or criminal penalties, underlining the importance of due diligence and honesty in its deployment. Sellers are obligated to retain this documentation as proof of exempt sales, emphasizing the form's significance in the maintenance of accurate tax records.

Form |

Indiana Department of Revenue |

StateForm :19065 |

General SalesThx Exemption Certificate |

Indianaregisteredrelail merchantsand businesseslocatedoutsideIndianamay usethis certificate.The claimedexemptionmust be allowedby Indiana code. Exemption slatutesof other statesare not valid tbr purchasesfrom Indiana vendors.This exemption certilicate can not be issued for the purchase of lLili/iqg, Vehicles, Watercraft, or Ai/crafr. Pttrcha.sermust be registered with the Depafiment of Revenue or the appropriate taxing authorityofthe purchaser'sstateof residence.

Sales tax must be charged unless a!! information in each 6ection is fully completed by the purchaser. Purchasersnot able to provide all required informationmust pay the tax and may file a ctaim for refund(Form GA- I

Name of Purchaser

B u s i n e s s A d d r e s s |

C i t y |

P u r c h a s e rm u s t p r o v i d e m i n i m u m o f o n e I D n u n i b e r b e l c l w . t '

Provide your Indiana Registered Retail Merchant's Certificatc TID and LOC Number as shown on your Certificate .

If not registered with the Indiana DOR, provide your State Tax I D N u m b e r f r o m a n o t h e r S t a t e . . . . . .

*See instructions on the reverse side if vou do not have either number .

State _ |

Zip |

T I D # ( l 0 d i g i t s ) |

LOC# ( 3 digits) |

SrarelD# |

Stateof Issue |

HI s t h i s a I b l a n k e t p u r c h a s ee x e m p t i o n r e q u e s to r a I

D e s c r i p t i o no f i l e m s t o b e p u r c h a s e d .

s i n g l e p u r c h a s ee x e m p t i o n r e q u e s t ? ( c h e c k o n e )

Purchasermust indicatethe lype oI exemptionbeing claimedfor this purchase.(checkone or explain)

E

E

E

E

Salesto a retailer,wholesaler,or manufacturerfor resaleonly.

Saleof manufactu ng machinery tools.andequipmentto be useddirectly in direct production.

Salesto nonprofft organizations claimingexemptionpursuantto SalesTax lnformationBullelin #10. (May not be usedfor personalhotel roomsand meals.)

Salesofrangible personalpropertypredominatelyused(greaterthen50 percent)in providing public transportation - provide USDOT#.

Apersonor corporalionwho is baulingundersomeoneelse'smotor carrierauthority,or hasa contractasa schoolbus operator, must providc their SS#or FID# in lieu of a StateID# in Section#1. USDOT# -

E

E

E

Salesto persons,occupationallyengagedasfamers, to be useddirectly in productionof agricultural productsfor sale. Note: A farmernot possessinga StateBusinessLicense#may entera FID# or a SS# in lieu of a StateID# in Section#1.

Salesto a contractor for exemptprojects(suchaspublic $chools,or nonprofits). Sovemment,

Salesto Indiana Governmental Units (agencies,cilies,towns.municipalities,public schools,and slateuniversities).

El

Salesto the United States Federal Government - show agency name .

Note: A U . S . Government asencv should enter its Federal Identification Number (FID#) in Section #1 in lieu of a State ID# .

E O t h e r - e x p l a i n .

Iherebycerlify underthe penaltiesof perjury that lhe propeny purchasedby the useof this exemptioncertificateis to be usedfor an exempt purposepursuanlto theStateCrossRetailSalesTaxAct,

Iconfirm my undeBtandingthat misuse,(?ifrer egligentor intentioral), and/orfraudulentuseofthis certificatemay subjectboth me personally and/orthe businessentity I represenlto the impositionoftax, interest,and civil and/orcriminal penalties.

Signature of Purchaser |

Date |

Printed Name |

Title |

The Indiana Dcpartntent of Revenue may request verification of registration in another state if you are an out - of - state purchaser .

Seller must keep this certificate on file to support exempt sales.

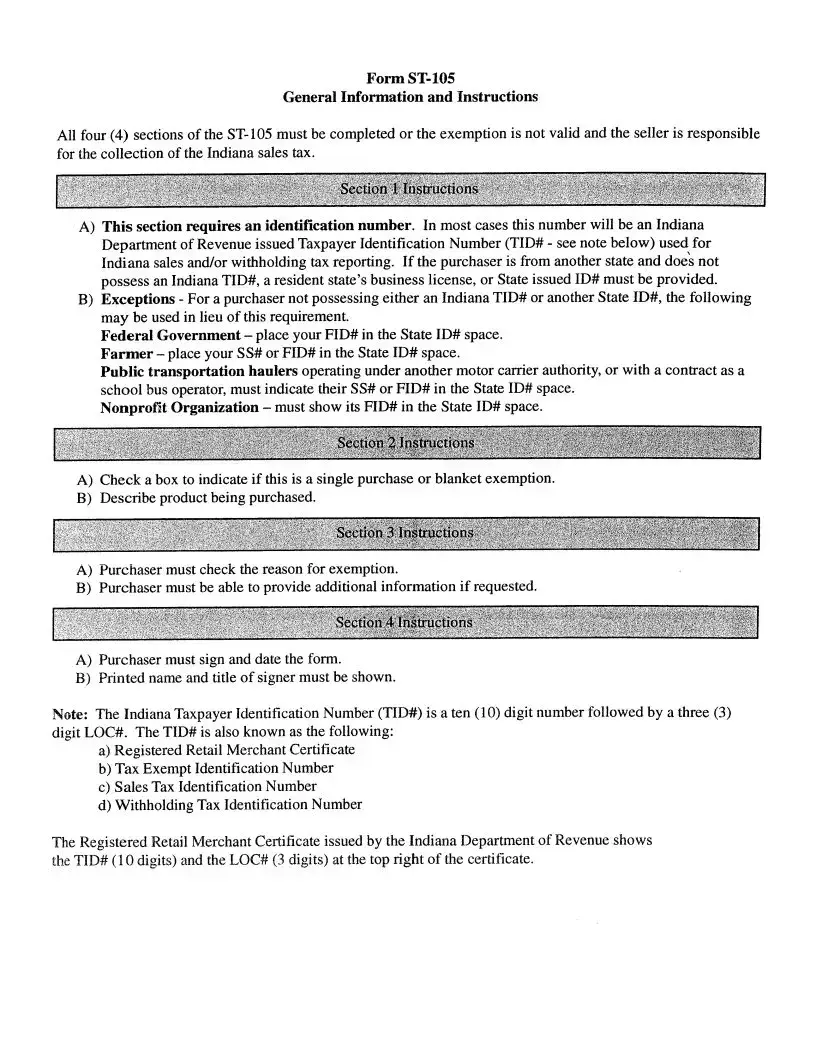

GeneralInfonnation and Instructions

All four (4) sectionsof

A)This sectionrequires an identification number. In mostcasesthis numberwill be anIndiana DeparunentofRevenueissuedTaxpayerldentificationNumber(TID# - seenotebelow) usedfor Indianasalesand/orwithholdingtax reporting. If the purchaseris from anotherstateanddoei not possessanIndianaTID#, a residentstate'sbusinesslicense,or StateissuedID# mustbeprovided.

B)Exceptions- For a purchasernot possessingeitheranIndianaTID# or anotherStateID#, thefollowing

may beusedin lieu of thisrequirement. tr'ederalGovernment- placeyourFID# in theStateID# space. Farmer - placeyour SS#or FID# in theStateID# space.

Public transportation haulersoperatingunderanothermotor carrierauthority,or witb a contractasa

schoolbusoperator,mustindicatetheir SS#or FID# in theStateID# space. Nonprolit Organization- mustshowits FID# in the StateID# space.

A)Check a box to indicateif this is a singlepurchaseor blanketexemption.

B)Describeproductbeingpurchased.

A)Purchasermustcheckthereasonfor exemption.

B)Purchasermustbe ableto provide additionalinformation if requested.

A)Purchasermust sign and date the form.

B)Printednameandtitle of signermustbe shown.

Note: The Indiana TlrxpayerIdentification Number (TID#) is a ten (10) digit number followed by a thtee (3) digit LOC#. The TID# is alsoknown asthe following:

a)RegisteredRetail Merchant Certificat€

b)Tax Exempt Identification Number

c)SalesTax Identification Number

d)Withholding Tax Identification Number

The RegisteredRetailMerchantCertificateissuedby the IndianaDepartrnentofRevenueshows the TID# ( I 0 digits) and the LOC# (3 digits) at the top right of the certificate'

| Fact Number | Detail |

|---|---|

| 1 | The Form ST-105 is issued by the Indiana Department of Revenue for sales tax exemption purposes. |

| 2 | It is designed for use by Indiana registered retail merchants and businesses located outside Indiana. |

| 3 | The exemption claimed must comply with Indiana code, and statutes from other states do not apply. |

| 4 | This certificate cannot be used for the purchase of utilities, vehicles, watercraft, or aircraft. |

| 5 | All four sections of the ST-105 form must be fully completed for the exemption to be valid. |

| 6 | The Indiana Department of Revenue may request verification of registration from out-of-state purchasers. |

| 7 | There are specific ID requirements outlined by the form, including Indiana TID#, out-of-state ID, or specific exceptions like FID# for federal organizations and SS# for farmers. |

| 8 | Governing law for this form is the Indiana Gross Retail Sales Tax Act, under Indiana Code 6-2.5. |

Filling out the Indiana ST-105 form is a straightforward process that necessitates attention to detail to ensure that all applicable exemptions are accurately claimed. This document is essential for Indiana registered retail merchants and businesses located outside Indiana aiming to purchase goods without paying state sales tax. The completion of this form requires providing specific business information and reasons for the sales tax exemption claim. It's crucial to understand that any exemption claimed needs to be allowed by Indiana Code; exemptions from other states will not apply. Prior to starting, reviewing all sections and having all necessary information on hand will streamline the process.

Once completed, this form acts as a declaration of intent to make exempt purchases under the specified conditions. Sellers must keep this certificate on file to support exempt sales. It's worthwhile noting that misuse of this certificate, whether through negligence or intentional fraud, can lead to penalties, including tax liability, interest, and possibly civil or criminal actions. Therefore, filling out this form accurately and truthfully is paramount. Furthermore, the Indiana Department of Revenue may request verification of registration in another state for out-of-state purchasers, emphasizing the need for accurate and verifiable information.

What is Form ST-105 and who uses it?

Form ST-105 is the General Sales Tax Exemption Certificate used in Indiana. It is utilized by Indiana registered retail merchants and businesses located outside of Indiana for purchasing items without paying sales tax. The form is necessary when the purchased items are for resale, manufacture, non-profit activities, or other qualified exemptions as defined by Indiana code. The claimed exemption must align with Indiana's statutes, as exemptions from other states are not valid for purchases from Indiana vendors.

Can Form ST-105 be used for purchasing anything tax-exempt?

No, there are specific restrictions on the use of Form ST-105. It cannot be issued for the purchase of utilities, vehicles, watercraft, or aircraft. The form is primarily designed for items that will be resold, used in manufacturing, provided to non-profit organizations, or used in qualifying exempt activities as outlined by the state. Users must ensure their purchases align with the exemptions allowed under Indiana code.

What information must be provided on Form ST-105?

To complete Form ST-105, purchasers must provide their business name, address, and at least one identification number—either the Indiana Registered Retail Merchant's Certificate TID and LOC Number or a State Tax ID Number from another state. Also, the form requires the purchaser to indicate whether the exemption is for a single purchase or a blanket exemption, describe the items to be purchased, and specify the type of exemption claimed. All sections of the form must be completed for the exemption to be valid, including the signature of the purchaser and the date.

What if a purchaser does not have any ID number required on Form ST-105?

If a purchaser does not possess an Indiana Department of Revenue issued Taxpayer Identification Number (TID#) or a State ID# from another state, there are specific exceptions allowed. Federal Government entities can use their Federal Identification Number (FID#), farmers can enter an FID# or SS#, public transportation haulers or contracted school bus operators can indicate their SS# or FID#, and non-profit organizations must show their FID#. These exceptions enable entities without a traditional State ID# to claim exemption when applicable.

Is a purchaser always exempt from sales tax if they submit a completed Form ST-105?

Not necessarily. The completion and submission of Form ST-105 indicate the purchaser's intent to buy goods tax-exempt for reasons authorized by Indiana law. However, the purchaser's eligibility and the nature of the goods or services bought must strictly comply with Indiana's exemption statutes. If a purchase does not meet these criteria, the exemption is not valid, and sales tax should be paid. Fraudulent use of this certificate can lead to penalties, including tax liabilities, interest, and possibly criminal charges.

How long should the seller keep Form ST-105 on file?

Sellers are required to keep completed Form ST-105 certificates on file to support exempt sales. While the document does not specify a retention period, it is generally recommended for businesses to retain sales tax exemption certificates and related records for at least seven years to comply with tax audit requirements and to verify the legitimacy of tax-exempt transactions.

Can anyone claim exemption by simply filling out Form ST-105?

No, only eligible businesses or organizations that meet specific criteria set by Indiana can claim an exemption using Form ST-105. The form serves as an affidavit where the purchaser certifies that the items bought are for qualifying exempt purposes. Claiming a fraudulent exemption knowingly can result in significant consequences, including repayment of tax, additional interest, penalties, and legal action. Therefore, it is imperative to understand and comply with the exemption qualifications as described by Indiana law.

When filling out the Indiana ST-105 form, a General Sales Tax Exemption Certificate, individuals and businesses frequently make errors that can invalidate their exemption or lead to compliance issues. Recognizing and avoiding these common mistakes is crucial for ensuring the process goes smoothly and correctly. Here are nine common mistakes:

It's important for purchasers to carefully read and follow the instructions provided with the ST-105 form to ensure they are in compliance with Indiana's sales tax exemption requirements. Diligence in completing the form correctly helps avoid any potential issues with tax exemption claims, safeguarding both the purchaser and seller from unnecessary complications.

When handling sales tax exemption in Indiana, specifically with Form ST-105, various other documents and forms might also be utilized to ensure compliance with tax laws and regulations. Here's a look at five additional documents often used alongside Form ST-105, each serving its unique purpose in the documentation and verification process.

Understanding and accurately completing these forms and documents ensures legal compliance and facilitates the efficient processing of sales tax exemptions in Indiana. This not only aids businesses in managing their fiscal responsibilities effectively but also aligns with the state's requirements for transparency and accountability in tax-related matters.

The Indiana ST-105 form, known for its role in sales tax exemption certification, bears resemblance to several other documents aimed at similar tax-exemption purposes across various states. Each analogous form serves as a testament to the structured way states manage sales tax exemptions for goods sold or purchased for specific uses exempt under the law. However, it's crucial to understand the nuances that distinguish the Indiana ST-105 form from its counterparts.

The Multistate Tax Commission’s Uniform Sales and Use Tax Certificate is an example of a similar document to Indiana's ST-105 form. The Multistate Certificate facilitates the exemption process for vendors operating in multiple states, offering a blanket approach to exemption certification. Like Indiana's ST-105, the Multistate Certificate requires identifiable information about the purchaser and details regarding the exemption claimed. The fundamental similarity lies in their objective to streamline tax-exempt purchases by qualifying businesses, albeit the Multistate form's broader geographical application contrasts with the ST-105’s specific use within Indiana.

The California Resale Certificate (BOE-230), while serving a different jurisdiction, mirrors the Indiana ST-105 in purpose and structure. Both forms are designed to certify that the purchaser intends to resell the purchased property in the course of business, thus rendering the transaction exempt from sales tax. The requirements for detailed information about the purchaser, the nature of the exemption claimed, and the acknowledgment of certain liabilities for misuse are shared attributes. However, the California Resale Certificate specifically caters to the resale market, highlighting a more niche focus compared to the broader exemption categories addressed by the ST-105.

Florida’s Annual Resale Certificate for Sales Tax is another document sharing similarities with Indiana’s ST-105 form. Like the ST-105, Florida’s certificate allows businesses to make tax-exempt purchases or rentals of property and services that will be resold or re-rented. Both documents necessitate that the purchaser provide identification and certification that the goods are intended for resale. The key distinction lies in the annual issuance of Florida's certificate, simplifying the process for frequent purchasers, whereas Indiana's ST-105 may require more frequent validation for each exempt purchase transaction.

When completing the Indiana ST-105 form, there are vital steps to follow and mistakes to avoid in order to ensure that the form serves its intended exemption purposes correctly. Below are 10 guidelines to assist you:

Following these guidelines will help ensure that the process is smooth and legally compliant, allowing businesses and organizations to properly claim the exemptions for which they are eligible.

Understanding the Indiana ST-105 form requires careful attention to its specific requirements and prevalent misconceptions. Misunderstandings can lead to incorrect application of sales tax exemptions, potentially causing legal and financial complications for both purchasers and sellers. Here are four common misconceptions about the Indiana ST-105 form:

Correctly understanding these aspects of the Indiana ST-105 form is crucial for both purchasers and retailers to navigate tax exemptions effectively. Misinterpretations not only lead to unsuccessful exemption claims but may also result in tax liabilities and penalties. Therefore, thorough familiarity with the form's instructions and legal requirements is paramount for its proper utilization.

Filling out and using the Indiana ST-105 form correctly is essential for businesses to qualify for sales tax exemptions on eligible purchases. Here are key takeaways to ensure compliance and proper usage of the form:

Understanding and adhering to these guidelines when filling out the Indiana ST-105 form can help ensure compliance, prevent legal issues, and potentially save your business from unnecessary tax expenses.

Eviction Notice Indiana - A legal pathway for landlords to demand the swift return of their property and settle issues of outstanding rent through the Henry Circuit Court No. 3.

Land Contract Indiana Pdf - Marks the official acknowledgment of the contract by a notary public, including a designated space for the notary's commission expiry date.

Indiana Personal Property Tax Forms - Penalties for filing inaccuracies include monetary fines and increased tax liabilities.