Indiana St 103Dr PDF Form

Indiana St 103Dr PDF Form

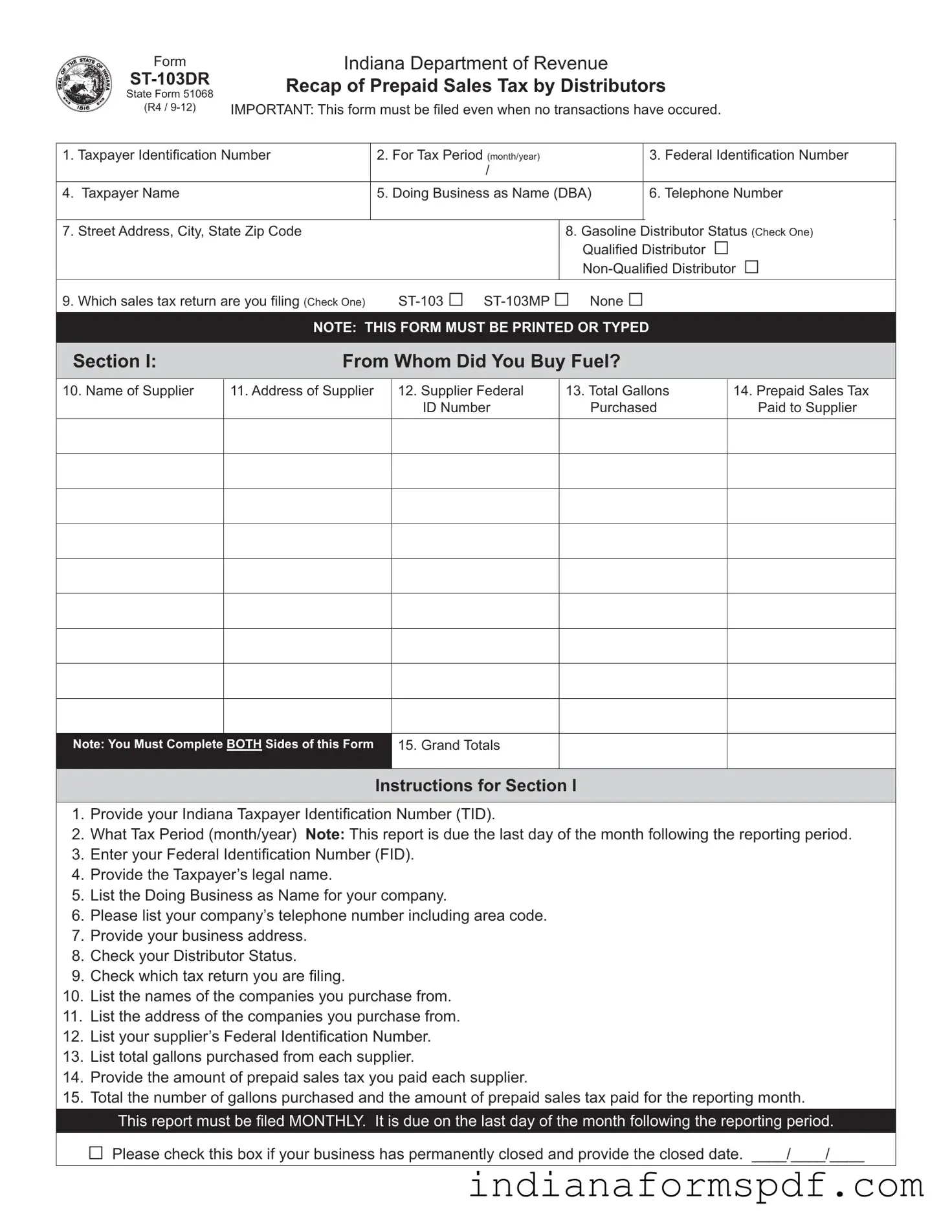

Navigating the complexities of tax reporting can be challenging for gasoline distributors in Indiana, but the ST-103DR form, officially titled Recap of Prepaid Sales Tax by Distributors, simplifies this process significantly. This pivotal document, as outlined by the Indiana Department of Revenue, is mandated for completion and submission by distributors to accurately report their prepaid sales tax activities. Key details such as the Taxpayer Identification Number, tax period, and the distributor's legal and doing business as (DBA) names form the foundation of the report. What sets the ST-103DR apart is its detailed requirement for listing transactions of both purchasing from suppliers and sales to customers, along with the prepaid sales tax paid or collected in these transactions. Notably, the form is designed to be comprehensive, including sections for the amount of fuel purchased and sold, the gallons exempt from tax, and the total prepaid sales tax involved. Importantly, this form must be filed monthly, due by the last day of the following month, and requires diligent attention even in periods where no transactions occur. Additionally, it encompasses a declaration of the accuracy and completeness of the report under penalty of perjury. The obligation to file this document, coupled with the specific information it gathers, underscores its significant role in the regulatory and fiscal landscape of Indiana’s fuel distribution sector.

|

Form |

|

Indiana Department of Revenue |

|

|||

|

Recap of Prepaid Sales Tax by Distributors |

||||||

|

State Form 51068 |

||||||

|

|

|

|

|

|

|

|

|

(R4 / |

IMPORTANT: This form must be fi led even when no transactions have occured. |

|||||

|

|

|

|

|

|

||

1. Taxpayer Identifi cation Number |

|

2. For Tax Period (month/year) |

|

3. Federal Identification Number |

|||

|

|

|

|

/ |

|

|

|

|

|

|

|

|

|

|

|

4. |

Taxpayer Name |

|

|

5. Doing Business as Name (DBA) |

|

6. Telephone Number |

|

|

|

|

|

|

|

||

7. |

Street Address, City, State Zip Code |

|

|

8. Gasoline Distributor Status (Check One) |

|||

|

|

|

|

|

Qualifi ed Distributor □ |

||

|

|

|

|

|

|||

9. |

Which sales tax return are you filing (Check One) |

|

|||||

|

|

|

NOTE: THIS FORM MUST BE PRINTED OR TYPED |

|

|||

|

|

|

|

||||

Section I: |

|

From Whom Did You Buy Fuel? |

|

||||

10. Name of Supplier

11. Address of Supplier

12.Supplier Federal ID Number

13.Total Gallons Purchased

14.Prepaid Sales Tax Paid to Supplier

Note: You Must Complete BOTH Sides of this Form

15. Grand Totals

Instructions for Section I

1.Provide your Indiana Taxpayer Identifi cation Number (TID).

2.What Tax Period (month/year) Note: This report is due the last day of the month following the reporting period.

3.Enter your Federal Identifi cation Number (FID).

4.Provide the Taxpayer’s legal name.

5.List the Doing Business as Name for your company.

6.Please list your company’s telephone number including area code.

7.Provide your business address.

8.Check your Distributor Status.

9.Check which tax return you are filing.

10.List the names of the companies you purchase from.

11.List the address of the companies you purchase from.

12.List your supplier’s Federal Identification Number.

13.List total gallons purchased from each supplier.

14.Provide the amount of prepaid sales tax you paid each supplier.

15.Total the number of gallons purchased and the amount of prepaid sales tax paid for the reporting month.

This report must be fi led MONTHLY. It is due on the last day of the month following the reporting period.

□Please check this box if your business has permanently closed and provide the closed date. ____/____/____

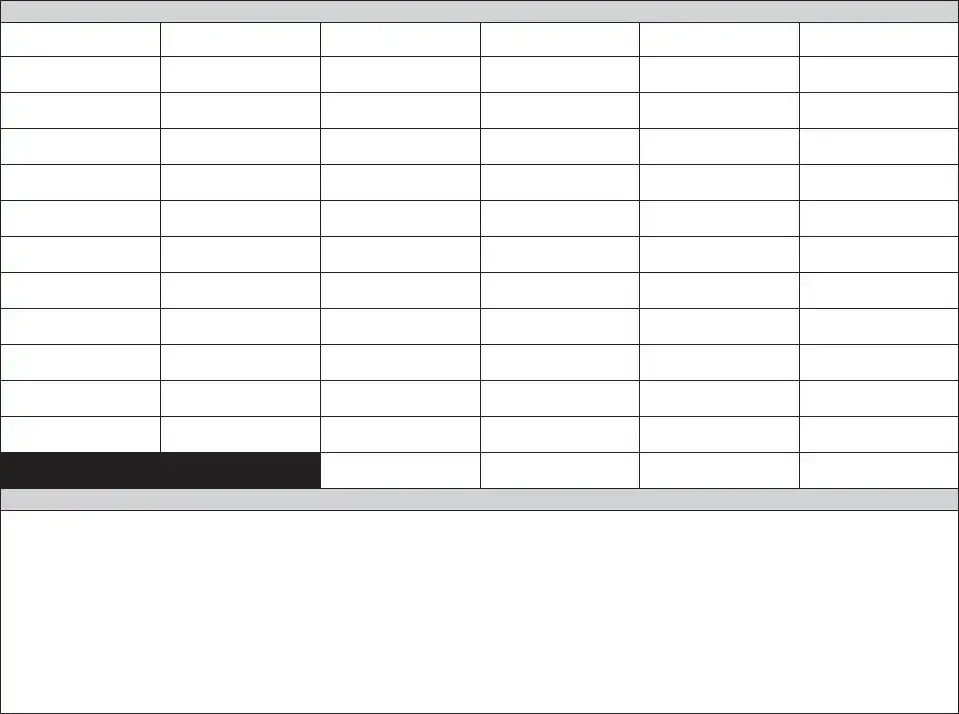

SECTION II |

To Whom Did You Sell Fuel? |

16. Customer’s Name

17. Customer’s Address

18.Customer’s Federal ID Number

19. Total Gallons Sold

20. Exempt Gallons Sold

21. Prepaid RST Collected

All Gallons EXEMPTED and TAXED must be shown

22. Total

Instructions for Section II

16.List your Customer’s Name. (Attach additional sheets if necessary).

17.List your Customer’s Address.

18.List your Customer’s Federal ID Number.

19.List the total gallons of gasoline sold for this month to each customer.

20.List the total tax exempt gallons sold to each customer.

21.List the total amount of Prepaid Sales Tax collected for this month from each customer.

22.Total the amounts of all columns and give the total gallonage and amount collected here.

I declare, under penalties of perjury that this is a true, correct and complete report.

Mail to: Indiana Department of Revenue Excise Tax

P.O. Box 6114 Indianapolis, IN

______________________________________________ |

_____________________________________________ |

__________________________ |

________________ |

Printed Name |

Authorized Signature |

Title |

Date |

| Fact | Description |

|---|---|

| Form Name | Indiana Department of Revenue ST-103DR Recap of Prepaid Sales Tax by Distributors |

| State Form Number | 51068 |

| Revision Date | R4 / 9-12 |

| Filing Requirement | This form must be filed even when no transactions have occurred. |

| Taxpayer Identification Needed | 1. Taxpayer Identification Number 2. Federal Identification Number |

| Business Information Required | Taxpayer Name, Doing Business as Name (DBA), Telephone Number, and Business Address |

| Distributor Status Options | Qualified Distributor, Non-Qualified Distributor |

| Tax Return Filing Options | ST-103, ST-103MP, or None |

| Report Sections | Section I: From Whom Did You Buy Fuel? Section II: To Whom Did You Sell Fuel? |

| Monthly Filing Requirement | This report must be filed MONTHLY and is due on the last day of the month following the reporting period. |

| Governing Law | Indiana state law regarding the collection and remittance of prepaid sales tax by fuel distributors. |

Filling out the Indiana ST-103DR form is an essential task for distributors to recap their prepaid sales tax. This form ensures accurate tracking and reporting of prepaid sales tax transactions. Here is a structured guide to help you navigate through and accurately complete the Indiana ST-103DR form.

By following these steps, you can ensure the accurate and timely submission of your report, maintaining compliance with Indiana's tax reporting requirements. Remember, this form is due monthly, no later than the last day of the month following the reporting period.

What is the purpose of the Indiana ST-103DR form?

The Indiana ST-103DR form is specifically designed for distributors to report and recap prepaid sales tax on gasoline purchases. Its primary purpose is to ensure that the correct amount of sales tax is collected and remitted to the state by distributors who buy and sell gasoline. By meticulously filling out this form, distributors declare the total gallons of gasoline purchased from suppliers, the prepaid sales tax paid on these purchases, and similarly detailed information for sales, including exempt transactions. This form plays a crucial role in maintaining transparency and compliance with state tax regulations, ensuring that the correct taxes are paid for gasoline distributions.

Who needs to file the Indiana ST-103DR form?

This form must be filed by all gasoline distributors operating within the state of Indiana, regardless of their distributor status as either qualified or non-qualified. It is specifically tailored for those in the business of buying and selling gasoline who are subject to collecting prepaid sales tax on these transactions. The requirement to file this form applies even if no transactions occurred during the reporting period, highlighting its importance in maintaining up-to-date records with the Indiana Department of Revenue.

When is the Indiana ST-103DR form due?

The Indiana ST-103DR form is due monthly, with the deadline set for the last day of the month following the reporting period. This means, for instance, if you are reporting for the month of January, your completed form should be submitted to the Indiana Department of Revenue by the last day of February. Timely submission of this form is crucial for distributors to avoid penalties and ensure compliance with state tax obligations. It is a regular and ongoing requirement that reflects the distributor's operations for the preceding month.

What happens if no transactions occurred during the reporting period?

Even if no transactions occurred during the reporting period, gasoline distributors are still required to file the Indiana ST-103DR form. This is a critical aspect of compliance, as it ensures all distributors maintain consistent records with the Indiana Department of Revenue. Filing the form in periods of inactivity not only keeps your records up to date but also helps in avoiding any potential penalties for presumed non-compliance. Distributors should accurately complete the form indicating that no transactions took place to fulfill their reporting obligations.

Filling out the Indiana Department of Revenue ST-103DR Recap of Prepaid Sales Tax by Distributors form is a requirement for businesses dealing with fuel distribution in Indiana. However, common mistakes can lead to inaccuracies or even penalties. Here are seven errors often seen on this crucial form:

Avoiding these common mistakes requires careful attention to detail and an understanding of the form’s requirements. Here are some general tips to ensure accuracy and compliance:

By being mindful of these common pitfalls and following best practices for filing, businesses can successfully navigate the complexities of the ST-103DR form, ensuring compliance with Indiana’s tax regulations and contributing to a smoother tax filing process.

When filing the Indiana Department of Revenue ST-103DR form, also known as the Recap of Prepaid Sales Tax by Distributors, there are several other forms and documents that businesses commonly use in conjunction to comply with state tax regulations. These documents are essential for ensuring businesses meet all tax obligations accurately and on time.

Understanding the purpose and requirement of each of these forms is crucial for business owners and tax preparers. Proper completion and timely submission ensure compliance with Indiana's tax laws and help avoid penalties or audits. Businesses should always seek to remain informed about state tax requirements and any changes to the forms or related processes to ensure full compliance.

When completing the Indiana ST-103DR Recap of Prepaid Sales Tax by Distributors form, there are several key practices you should follow to ensure accuracy and compliance with state requirements. Equally, there are missteps you must avoid to prevent errors or potential legal issues. Below are essential dos and don’ts to consider.

Do:

Don’t:

Understanding the ST-103DR form, issued by the Indiana Department of Revenue, can sometimes be confusing. This form is essential for distributors, particularly those dealing with gasoline, as it addresses the recap of prepaid sales tax. However, several misconceptions often arise regarding its completion and purpose. Let's clear up some of these misunderstandings.

It's only for gasoline distributors: While gasoline distributors primarily use the ST-103DR form, it applies to all distributors required to report and pay prepaid sales taxes to the Indiana Department of Revenue.

Filing is only necessary when transactions occur: A common misconception is that you only need to file the ST-103DR form when there are transactions to report. However, the form must be filed for each period, even if no transactions occurred.

It's an annual report: Some may think the ST-103DR is an annual report. Actually, it's a monthly requirement. Distributors must file it by the last day of the month following the reporting period.

Electronic filing isn't an option: Many believe that the ST-103DR form must be printed and mailed. While it can be mailed, distributors also have the option to file electronically, streamlining the filing process.

Prepaid sales tax details are not crucial: Every detail about prepaid sales tax is crucial. This includes the amount of prepaid sales tax paid to each supplier, as well as the total gallons purchased. These details ensure accurate reporting and compliance.

Information about sales is optional: The second section of the form requires detailed information about fuel sales, including customer details and the amount of prepaid sales tax collected. This is not optional but a mandatory part of the filing process.

Additional sheets aren’t allowed: If you run out of space, it is entirely permissible to attach additional sheets with the required information for both the purchasers and customers. This ensures complete and accurate reporting.

It serves the same purpose as regular sales tax returns: The ST-103DR form has a specific purpose, which is different from regular sales tax returns. It focuses on the recap of prepaid sales taxes by distributors, ensuring that taxes on fuel purchases and sales are accurately reported and paid.

Penalties for late filing are negligible: Failing to file the ST-103DR form on time or submitting an incomplete or incorrect form can result in penalties. It's important to adhere to deadlines and ensure the form is filled out correctly and completely.

Clarifying these misconceptions helps in understanding the importance of the ST-103DR form and ensures distributors are compliant with Indiana's reporting requirements. Always ensure that you're up to date with the latest forms and guidelines from the Indiana Department of Revenue to avoid any compliance issues.

Filling out and using the Indiana ST-103DR form, which recaps prepaid sales tax by distributors, involves several key steps and points of attention. Here are some essential takeaways to ensure accuracy and compliance:

Overall, proper completion and submission of the Indiana ST-103DR form is a critical component of a gasoline distributor's tax obligations. By following these key takeaways, distributors can ensure they meet their responsibilities accurately and efficiently.

When the Inspection Report Comes In, Which of the Following Should a Buyer's Agent Do? - Facilitates a mutually agreed upon resolution to any property condition concerns raised during the inspection, aiding in sale progression.

New Indiana Paternity Laws - It serves as a formal recognition of paternity without the need for a court order, streamlining the process for unmarried parents.